The SmallTrades investment portfolio {appended} is actively managed to seek large profits from the stock market. The goal is to exceed the U.S. Stock Market’s returns by investing in an exchange-traded stock-index fund {ETF} and a select group of stocks. The stock market’s returns are measured by a benchmark index named the Standard-and-Poors 500 Total Return index.

History

In past years, the portfolio returns generally underperformed the benchmark returns for reasons explained in the Annual Report for 2021. The magnitude of underperformance is graphically displayed in figure 3 of the 2021 Annual Report. After 14 years, the portfolio’s compound annual growth rate reached 4% compared to the benchmark’s 11%.

Today

The portfolio is now 15 years old. This is a report of the investment outcome of year 15. Figure 1 below displays the outcome as a series of annual rate-of-returns for the benchmark index [black bars] compared to the portfolio [blue bars] and portfolio assets [red and yellow bars].

Figure 1: Annual returns.

Figure 1 shows frequent gains above 0% during the 6th to 14th years with exception of the years 11 and 15. In year 15, the benchmark’s annual rate of return fell -18% [black bar in figure 1]. The portfolio fell -24% [blue bar], ETF declined -38% [yellow bar], and the stocks collectively rose +40% [red bar]. The remainder of this report will describe the events and partial success of year 15.

Remodeled portfolio

The strategy for year 15 was to reinvest in a growth-index ETF and increase the investment in stocks.

Figure 2: Market values.

Figure 2 summarizes the remodeling process by displaying bar graphs of monthly portfolio market values. The height of each stacked bar graph represents a monthly portfolio market value comprised of stocks [blue bar], ETF [green bar], and cash [black bar]. Changes in the bar heights for January, February, and March represent the remodeling process. To begin the process, December 2021’s ETF [SCHX] was replaced in January by a smaller investment in the growth-index ETF [SCHG]. I also sold 3 stocks [trading symbols NKLA, NVEC, RKLB] to collect extra cash. January’s cash was used to buy shares of stocks in February and March. In February, I purchased 3 stocks [trading symbols SMED, META, MKSI] plus additional shares of existing stock holdings. The effects of trading were essentially complete by the end of March. Excluded from figure 2 are the cash dividends of various holdings and privatization of SMED during April through November. Cash dividends were selectively invested in stock shares while SCHG’s dividends were automatically reinvested. Over the last ten months of year 15, the percentage market values of portfolio assets fluctuated between 28-33% stocks, 70-66% SCHG, and 1% cash. During that same time period, the allocation of principal held steady at 1% cash, 24% stocks, and 75% SCHG. By December 31, 2022, the up-trending blue bars in figure 2 indicated that the portfolio’s remodeled group of stocks sustained its increased market value despite shrinkage of SCHG’s market value.

Analysis of Year 15

If monthly variations in market value are firmly linked to stock market fluctuations, there should be no difference between percentage market values of the portfolio assets and benchmark index. Otherwise, the differences would diverge with the passage of time

Figure 3: Relative returns.

Figure 3 is derived from figure 2’s monthly market values of the stocks [blue bar] and ETF [green bar] compared with historic changes of the benchmark index [gray bar]. The monthly market values in 2022 are re-plotted as percentages of the initial market values on December 31, 2021; “100%” represents the initial market values. The remodeling process in January-March of 2022 created a remarkable divergence of percentage market values with the portfolio’s stocks rising above 100% while the ETF and benchmark dropped below 100%. After the remodeling period, stock market dynamics further reduced the market values of the ETF and benchmark index below their initial 100% without reducing the 140% gain of the portfolio stocks. In other words, the net effect of active stock trading in the first quarter endured year 15’s Bear market.

Plan for 2023

A pessimistic economic forecast for 2023 might entice other market participants to retreat from the stock market. I plan to hold fast by maintaining my current 75/25 allocation of investment principal and maintain a long position on portfolio holdings.

The sword of inflation ‘slices’ cash and credit away from consumer spending. The latest rise of inflation rates, from 2% before 2021 to above 8% in 2022, reduces the purchasing power of money. Consider today’s dollar, which buys 25% less gasoline compared to one year ago. Relentless inflation causes families to either spend more income, withdraw more savings, or borrow money to pay higher costs of living.

Borrowers with good credit ratings are expected to repay loans with interest in a timely fashion. The Federal Reserve is currently increasing the difficulty of borrowing money [i.e., ‘tightening credit’] by raising the interest rates of loans. Corporations will eventually produce fewer goods and services in response to regulatory tightening of the credit needed to buy supplies and pay wages. Reduction of corporate productivity threatens stock returns and economic recession.

The rate of return from a stock investment, –or any other financial investment–, measures the face value [i.e., “nominal” value] of the investment’s profit; but the “real rate of return” measures the purchasing power of the profit. Inflation lowers the real rate of return, which reduces the purchasing power of a profit. The effect of a bear market on investment profit is bad enough; inflation adds an additional strain to profitability.

One of the biggest risks of investing is that of encountering the inevitable “bear market” during a market cycle. Today’s stock market descended into a ‘bear market’ on June 13th, 2022, when the market index fell by 21% below its previous ‘high’. My SmallTrades portfolio fell by 26% over the same time period [Fig. 1].

Fig.1 bear market

Figure 1 shows a greater loss of market value in the portfolio, compared to its index, due to losses incurred by the portfolio’s holdings. Here’s what happened:

In January, 2022, last year’s broad market ETF [ticker SCHX] and two stocks with disappointing share prices [tickers NVEC and NKLA] were replaced by a growth sector ETF [ticker SCHG] and three established stocks [tickers FB, MKSI, and SMED]. Residual cash was added to several stocks as needed to equalize the distribution of stock investments. Consequently, the distribution of invested principal shifted from 80% ETF-20% stocks to 70% ETF-30% stocks in three months. Figure 2 illustrates the sequential transfer of cash from the ETF to the stocks [Fig. 2].

Fig. 2 reallocation

Meanwhile, a market-wide decline in prices diminished the market value of my portfolio over the entire six-month period [Fig 3].

Fig. 3 impact

All relative values started at 1.00 on December 31st and subsequently changed due to the combined effects of portfolio revision combined with the 6-month onset of the ‘bear market’. Parallel declines of unit values in the stock market (black line), portfolio (red line), and ETF (green line) are consistent with a general downward trend of share prices driven by pessimistic trading in the stock market. A transient surge of my stock values (blue line) reflects infusions of cash into several stock investments during the first 2 months of portfolio revision.

Delistings might add to losses during the ‘bear market’. Suppose two of my stocks with the worst market performance were delisted on June 1st. Estimated losses of -5.1% stock value and -1.6% portfolio value would deepen the June 13th losses described in figure 1. The diversification of my stock investments protects from a steeper loss caused by any delistings. Hopefully my portfolio will remain intact in the near future and recover its growth trend after the “2022 bear market“.

My private SmallTrades Portfolio is a Roth Account in which I no longer make annual contributions and cash withdrawals. Calendar year 2021 marked the 14th year of active portfolio management. Figure 1 shows the latest portions of year-end market value as 81% index-ETF, 18% U.S. stocks, and 1% money market.

Fig 1.

Annual returns

My investment goal is to earn an annual rate of return above that of the benchmark Standard & Poors 500 Stock Index. Unfortunately, the Portfolio usually underperforms the Benchmark.

Fig 2.

Figure 2 presents the history of annual returns for the Portfolio (blue bars), portfolio holdings (yellow & red bars) and Benchmark (black bars). In year 14, the Portfolio earned a 27% rate of return compared to the Benchmark’s 29% rate of return, thus underperforming the Standard & Poors 500 Index by a margin of 2%. The history of annual returns reveals devastating losses of market value in the first 6 years followed by encouraging gains in the last 8 years. Speculation and hurried trading, augmented by the 2008 Recession in year 1, created multi-year losses. After year 6, reduced speculation and slower trading produced multi-year gains.

14-year growth

Devastating losses of Portfolio value in the first 6 years precluded any chance of matching the cumulative growth of the Benchmark over 14 years.

Fig. 3.

Figure 3 displays the cumulative growth of annual returns as a chain of “unit” market values. The unit market values of the portfolio (blue dots) are ratios of year-end market value to the initial market value at time 0. After 14 years, the Portfolio’s compound annual growth rate reached 4% compared to the Benchmark’s 11%.

8-year growth

To evaluate the cumulative growth of annual returns in the last 8 years, I reset the unit value to $1.00 at the end of year 6 and recalculated the succeeding unit values now displayed in figure 4.

Fig. 4.

Less speculation coupled with longer holding periods enabled Stocks (red dots) to outperform the Benchmark (black dots) through year 10 and generally outperform the Portfolio (blue dots). The Portfolio (blue dots) matched the performance of its ETF (yellow dots).

Summary

Measurements of annual return and cumulative growth show that the SmallTrades Portfolio continues to underperform its Benchmark by a wide margin of 7% cumulative growth over 14 years. The last 8 years produced encouraging results based on improvements in portfolio management. To continue improving, but not wishing to leverage my investments, my choices are to invest in a growth index ETF and/or re-allocate assets to a higher portion of growth stocks in the portfolio.

After investing in mutual funds for several years, I began trying to earn an exceptionally high return of 30% in future years by trading profitable stocks in short periods of time. Could I outperform the stock market with short term trading?

Short-termism is the habit of selling securities in the stock market after brief periods of ownership less than one year. My short-termism is summarized in figure 1 for the past thirteen years. According to the gold and green bar graphs, more short term than long term sales were made during the first ten years. The gold dashed line shows a steady decline of 3-year moving averages for short term sales after the eighth year. By the thirteenth year, the average number of short term sales fell below the average number of long-term sales (green dashed line). The portfolio’s average number of year-end securities (blue dashed line) varied between 17 and 20 after the fifth year.

Figure 1 legend. The annual numbers of short-term sales (gold bars), long-term sales (green bars), and year-end holdings (blue bars) are represented by the height of the bars. Dashed lines represent those numbers as 3-year moving averages. Each moving average is an average of the previous 3 years.

I compared my portfolio to the stock market using the “percentage return” measurement shown below in figure 2. Heights of the bar graphs for the portfolio (blue) and stock market (black) changed according to the percentage change in market prices between the start and finish of the year. Goal lines for “30%” and “-30%” represent exceptional gains and losses. At the end of 2008 (“year 1”) the portfolio lost 60% of its starting value compared to the market’s 37% loss. During year 2, my successful trading in the resurgent stock market lifted the portfolio’s percentage return by 54%. But successful trading had nothing to do with the portfolio’s 123% return in year 3. Instead, I made a one-time transfer of additional stocks into the portfolio from another investment account. Thereafter, with the exception of year 11, the stock market outperformed the portfolio as indicated by higher percentage returns. Short term sales (gold bars) accounted for the portfolio returns of years 1, 2, and 5, but otherwise failed to account for the portfolio returns [nor did long term sales (green bars); unsold securities usually accounted for most of the percentage returns].

Figure 2 legend. “Percentage return” of the “portfolio” and “market” represents the change in total value for each entity at the beginning (value1) and end (value2) of one year [return = 100(value2 – value1)/value1]. “Percentage return” of sales represents the net profits of “short-term sales” and “long-term sales” earned during the year as percentages of total portfolio value at the end of the year. The investment goal of 30% return is represented by the upper black line.

Figure 3 (below) clearly shows that my portfolio failed to achieve the goals of earning a 30% CAGR and outperforming the stock market. The portfolio’s thirteen-year CAGR of 7.9% was 1.9 percentage points below the stock market’s 9.8% CAGR and 22.1 percentage points below the desired 30% CAGR. In terms of cash value, a $1,000 sample of baseline investment ultimately grew to $2,690 in the portfolio (blue line) compared to $3,370 in the stock market (black line). At the stated “30% target” growth rate (dashed line), every $1,000 invested at baseline would theoretically grow to $4,000 in merely 5 years. The portfolio’s final surge in the last two years came from reinvesting 80% of the total value into an index fund that tracks the stock market.

Figure 3 legend. “Multiple” is the ratio of year-end value to baseline value. Baselines of the “Portfolio” and “Market” occurred at the close of trading in 1979 (time 0). Year-end value of the “Market” was reported by the Standard and Poors 500 Total Return Index.Multiples below 1.0 are losses and above 1.0 are gains.

Short-termism wasn’t the only reason I failed to earn a 30% annual return, but I believe it is the main explanation; here’s why:

Fluctuating prices in the market prevent accurate timing of returns. Technical analysis of stock prices doesn’t guarantee accurate timing of trades.

The fundamental analysis of stocks for short term trading is costly in terms of time spent on research and subscription fees for research reports.

Frequent stock purchases can be an overwhelming task without the aid of an effective screening program and computer-assisted analyses. A problem with screening programs is the slow turnover of attractive stocks over a period of months rather than weeks. I began to run out of new ideas after a few months.

A portfolio with too few or too many stocks is unlikely to beat the market. Underperformance of one or more stocks among a few securities incurs the burden of recovering losses before earning high returns. Too many stocks likely dilute the returns.

I lost the opportunity to earn higher returns by selling good stocks too soon. Behavior analysts offer the opinion that long term buy-and-hold strategies offer a better chance of earning annual returns than short term sales strategies.

Investing in distressed companies at low prices incurs an extended period of time needed for the company to recover its financial health and desired growth of earnings.

Cash is necessary to purchase new securities, but too much cash dilutes the profits from short-term trading [please see “cash penalty” in the Appendix].

Conclusion. Bad choices and hurried trading most likely explain my subpar performance. The worst choice was purchasing shares of LEH (the listing of Lehman Brothers Holdings Inc. in the New York Stock Exchange) in year 1 when respected analysts warned against investing in such a deeply indebted company [more explanation in the Appendix]. And, hurried trading is a risky business due to unpredictable pricings and unexpected market declines. It’s less risky to purchase undervalued stocks of good companies and wait for however long it takes to sell those stocks at overvalued prices. A collection of healthy stocks protects from the inevitable decline of some companies.

Appendix: My trading behavior

30% goal. A compounded monthly return of 2.25% should yield a 30% annual return, which produces a compound annual growth rate (“CAGR”) of 30% when repeated for a period of years.

Assumptions:

net monthly returns of 2.25%

Every sale is promptly replaced by a security that continues earning a monthly return of 2.25%.

Negligible ‘cash penalty’ [cash penalty: every dollar of uninvested cash doubles the required monthly return from the same amount of invested cash].

My strategy was to sell stocks above cost by analyzing price charts. Frequent trading produced mixed results during the first two years (figure 2). Several trades earned sizable short term profits, notably stocks listed as GOOG (19%) and SOHU (14%). Other trades earned disasterous short term losses, notably LEH (-27%), SOL (-26%), and NVDA (-35%). The 2008 Recession occurred during this time period and undoubtedly contributed to my 60% loss in year 1. Year 1 ended with a portfolio of 4 stocks and $15 (~0%) in cash. During year 2, successful trading in a resurgent stock market lifted the portfolio’s annual return by 54%. The year-end portfolio held 27% cash and 73% securities which were comprised of stocks and one real estate investment trust (REIT).

[case history #1, LEH: My worst investment occurred in 2008 when I ignored the signs of a troubled company named Lehman Brothers Holdings Inc. to purchase its stock at several levels of declining share prices. Instead of a profitable rebound, the declining stock was delisted from the market when the company filed for bankruptcy. I felt demoralized by the end of 2008]

[case history #2, GOOG & NVDA: Had I kept these stocks for thirteen years, my final returns-on-investment would be 283% (GOOG) and 3,415% (NVDA).]

In year 3, the one-time transfer of stocks from another account boosted my portfolio’s return by 123%. My intent was to acquire additional cash from short term sales in order to buy interesting securities such as exchange traded funds (ETFs). The ETFs offered a layer of protection against corporate bankruptcies and stock delistings. Short term trading of securities continued during years 3-5 with the inclusion of sector ETFs and leveraged ETFs. The portfolio held 19% cash, 34% stocks, and 47% ETFs at the end of year 5.

My revised goalin year 6 was to consistently outperform the market by combining market-matching returns using ETFs with above-market returns using stocks. I would do so with an 80% investment in ETFs and 20% investment in stocks. Promising stocks from foreign countries were added to the portfolio and leveraged ETFs were abandoned. The remaining ETFs were distributed among four different asset classes: 30% stocks, 30% REITs, 20% investment grade bonds, and 20% gold bullion. The occasionally rebalanced ETFs offered good protection at modest returns that underperformed the stock market.

In year 12, I sold the diversified group of ETFs to reinvest in a single broad-market ETF that mimicked the U.S. stock market. I no longer needed to rebalance the portfolio, with the added advantage of automatically reinvesting the fund’s dividends. The new ETF enabled the portfolio to match the stock market’s resurgence in years 12-13 (figures 2,3). The portfolio held 3% cash, 16% stocks, and 81% single-ETF at the end of year 13.

The SmallTrades Portfolio holds cash, one exchange-traded fund (ETF), and a folder of stocks (figure 1).

Figure 1.

Strategy

The SmallTrades investment goal is to earn an annual rate of return —as measured by percentage change of market value over the year— which surpasses the performance of the benchmark Standard & Poors 500 Stock Index. In figure 1, one index-ETF creates 80% of the Portfolio’s market value with an expectation of matching the benchmark’s rate of return. The stocks contribute 20% of the market value with an expectation of outperforming the benchmark’s rate of return.

Performance

During 2020, the SmallTrades Portfolio earned an 18.2% rate of return compared to the Standard & Poors 500 Index’s 18.4% rate of return, thus matching the benchmark’s performance. In figure 2, the 12-year trend of performance was considerably better for the benchmark than the portfolio. The benchmark’s 9.8% compound annual growth rate (CAGR) exceeds the portfolio’s 2.8% CAGR. Portfolio mismanagement explains its underperformance.

Figure 2. The unit value is a ratio of final-to-initial value. In this chart, the initial value was measured on 12/31/2007. Unit values less than 1.00 represent a loss and greater than 1.00 represent a gain.

In figure 3, the 7-year trend of performance was considerably better for the benchmark compared to the portfolio. The ETF performance coincided with that of the portfolio, indicating that the ETF is the major determinant of portfolio performance.

Figure 3. The unit value is a ratio of final-to-initial value. In this chart, the initial value was measured on 12/31/2013. Unit values less than 1.00 represent a loss and greater than 1.00 represent a gain.

Discussion

The “Great Recession” of 2007-08 devastated the Economy and the stock market as well as my portfolio. The effect of the “Recession” is seen in figure 2. The portfolio’s benchmark recovered higher and faster than it’s market value.

The stock market declined in the last quarter of 2018, which caused corresponding declines in market value of the portfolio’s ETFs and stocks (figure 3). That was a wakeup call to revise my investment strategy in 2019. First, I replaced the 4-sector group of ETFs (discussed in AR2018) with the current large-cap ETF (SCHW in fig 1). Second, I stopped using stop-loss orders to protect from losses and started using limit orders to capture large gains. The stop-loss orders focused on minimizing losses in a volatile market rather than seeking long-term gains. The result was a dramatic increase in performance of the portfolio, ETF, and stocks in 2019. The stock market crash of March 2020 and the Pandemic of 2020 combined to level the stock performance during 2020. I might have done better with different stocks, but that’s wishful thinking. Fortunately, the performace of the ETF protected the growth of my portfolio. My plan is to continue seeking long-term gains.

Long-term investors depend on their stocks to remain viable during economic recessions. In today’s Coronavirus Pandemic, businesses of all sizes are losing income from the forced reduction of consumer spending, which may destabilize companies to the brink of bankruptcy. Investors can assess stability by reviewing the financial health of their companies.

Financial health is the ability to pay all obligations in a timely matter. Credit ratings and analyst reports use propriety methods to measure financial health. You can independently rate the financial health of a public company using a single numerical score from 0 to 10 based on liquidity and solvency; the higher the score, the healthier the company (eq. 1).

equation 1: Health = Liquidity + Solvency

Liquidity

Liquidity refers to the ease of converting current assets into cash for payments of current liabilities. Current assets are considered convertible to cash within one year. Some assets are more liquid than others. Savings accounts, checking balances, money market funds, and receivables [i.e., customers’ IOUs] represent liquid assets. Inventory [i.e., unused supplies and unsold products] is considered an illiquid asset. Current liabilities are the costs of paying business expenses such as wages, payables, and intereston short-term credit. The following ratios provide useful measurements of liquidity:

Current ratio = Current assets / Current liabilities.

Quick ratio = (Current assets – Inventory) / Current liabilities

Interest coverage = EBIT / Interest [EBIT is the company’s earnings before accounting for the charges of interest and tax; EBIT is a measure of recurring income]

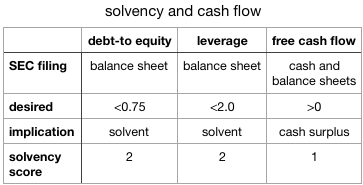

chart 1

Solvency

Solvency refers to the liquidation value of a company in case the company must pay all of its short-term and long-term liabilities. I use the shareholders’ equity [aka net worth or book value] as a common denominator for the measurement of solvency. Solvency ratios and free cash flow provide useful measurements:

Financial Leverage = Total assets / Shareholders’ equity.

Free Cash Flow = Operating cash flow – Capital expenses

chart 2

Examples

Chart 3 displays health scores for a list of companies identifiable by stock tickers; they are the current holdings of my investment club. The data were calculated with the formula in eq. 1 using open source data for liquidity and solvency. Three stocks received low health scores of 2.

chart 3

From chart 3, I selected five strong competitors of VZ and CMCSA to determine if the low health score represents a larger group of 7 competitors listed in the trading sector of Communication Services. The additional competitors are listed below in chart 4. Three of the additional competitors matched the scores of CMCSA and VZ, inferring that most companies in that select group operate with low liquidity and solvency.

chart 4

Another comparison was made using a sample of stocks with an open-source, proprietary grade of low financial health (chart 5). One stock, JCP, recently filed for chapter 11 bankruptcy.

chart 5

Risk management

The health scores in chart 3 are based on historical data at least 3 months old. Stocks with the lowest scores are considered more unstable. If, in your informed opinion, there’s a credible risk of bankruptcy and delisting, you can protect your investment by either selling the stock or placing a stop-loss order on it.

Conclusion

Open-source financial data can be used to assess the risk of potential bankruptcy and delisting among publicly traded stocks, especially during an economic recession. Combined assessments of liquidity (chart 1) and solvency (chart 2) additively form a health score of 0 to 10, with lower scores implying poor financial health. The scoring system is easy to implement, but unreliably predicts financial failure of public companies with low scores. Additional fundamental analysis of the company is strongly recommended and meanwhile, if you wish to protect your investment from a substantial loss, place a temporary stop-loss order on the holding.

The Stock Market is a place where professional traders arrange cash-for-stock transactions between buyers and sellers. Other securities are sold in the Market, but stocks occupy the vast majority of listed securities—(securities are investment contracts worth money, of which stocks represent shares of ownership in companies).

Every transaction is called a Trade. Regular trades involve the buyer’s payment of cash for securities offered by the seller. Buyers and sellers propose trades to their brokers who then send the proposals (orders) to professional traders. Market rules require traders to fill orders at the next available price, either the highest Bid of a buyer or lowest Ask of a seller, depending on the type of trade. The general trend of prices among many trades is calculated as the MarketIndex. Investors should prepare trading orders carefully with awareness of the potential consequences.

Competitive prices

The Stock Market is designed to set prices for securities at an agreeable price among competitive Bids and Asks –(the buyer’s price is called a Bid and the seller’s price is anAsk).The agreed price varies according to the prevailing action of trading orders in which Buy orders are filled at the lowest available Ask and Sell orders are filled at the highest available Bid.In a ‘seller’s market’, the buyers’ surplus demand for securities raises prices for the sellers. Examples include the rising prices in rallies and bull markets. In the ‘buyer’s market’, the sellers’ surplus supply of securities lowers prices for the buyers. Examples include the falling prices in corrections and bear markets.

Market Index

The Market Index is a singular value which represents the prices of many securities traded in stock exchanges [see index methodology in the appendix]. Graphs of the market index display daily fluctuations (volatility), trends, and market cycles. The trend of a market index is useful in several ways:

Analysis of supply-and-demand: An increased demand for shares drives prices upward and conversely, an increased supply of shares drives prices downward. The index follows the price trends.

Benchmark: Investors like to know if the prices of their holdings are performing better or worse than the market index.

Passive management: Index funds (e.g. ETFs) are investment portfolios designed to match the performance of an index.

Chart 1. The ‘Dow’ represents stock prices of 30 large companies traded in the New York Stock Exchange and Nasdaq market. The ‘S&P 500’ represents market capitalizations of 500 large companies traded in U.S. exchanges (market capitalization is the sum of prices for all shares of a given stock). The ‘Nasdaq’ is calculated from market capitalizations of all companies listed in the Nasdaq market.

Chart 1 displays the parallel behavior of 3 popular indices; they are broad market indices by virtue of describing the price volatility and trends of many stocks listed in the Market. Small fluctuations represent daily values reported at the close of the trading day. Large fluctuations display short and long cycles of market activity. Along market cycleconsists of one “bull” and “bear” market in succession. Long bull markets create a general upward trend of market prices that endures several market cycles.

Trading Orders

In contrast to the market index, which represents many stocks, the quote represents one stock. Quotes are widely published in the media and brokerage firms. A typical broker’s quote shows the last traded price, traded volume, and opposing prices (bid & ask).

Investors place a trading order by consulting their broker or employing the broker’s online trading platform.In a trading platform, the investor completes an order form with the following information:

Ticker.The trading symbol of the desired security

Action.Buy or Sell

Volume.Quantity of units (shares) to be traded

Type.Method for filling the order (Market versus conditional)

Price. conditional or Market.

The basic types of orders are Market and conditional. Market orders are filled immediately at the next available price, but the investor is unable to specify the price. Conditional orders enable the investor to specify the price of a future trade within a period called the “time-in-force” (typically 60 days). Conditional trades are activated at the specified price and filled at the next available price.

Limit and Stop are two types of conditional orders available to most stock investors. A Limit is the preferred price for a Buy or Sell order. The Limit order is activated when a future market price matches the Limit price. The activated trade is then filled at the same price or a more favorable price; but, if the next available price becomes unfavorable due to price fluctuation, the Limit order is cancelled unfilled. A Stop is the specified price of a Sell order. The Stop order is activated at the specified price and then filled by a Market order. The seller has no control of the price after a Stop order is activated.

A Trading Story

Two fictional investors named ‘Green’ and ‘Red’ decided to place opposite trading orders for the same security on March 5th when the quoted price was $49. ‘Green’ thought the price would eventually drop and wanted to buy 100 shares for a bargain at the Limit of $45. The intended bargain was a $400 reduction of investment cost. ‘Red’, who owned 100 shares, thought the future price would drop for a loss. “Red’ wanted to prevent a deep loss by selling 100 share at the $45 Stop. ‘Red’ would be happy if the Stop order were never activated, but just in case prices declined, the loss of $400 could be tolerated. The outcomes are illustrated in Chart 2.

Chart 2: The Fate of 2 Conditional Orders. Red and Green symbols represent respective Stop and Limit orders made on March 5th. The dashed line indicates that both orders remained-in-force until activated and filled on March 9th. An overnight crash of prices halted trading at the start of the March 9th trading day.

On March 9th, a market crash activated both orders at the moment trading was halted by a circuit breaker. When trading resumed, ‘Green’ bought 100 shares at the very favorable price of $41, even $4 cheaper than the intended $45 Limit. ‘Green’s’ bargain was $800 instead of $400. ‘Red’ sold 100 shares at the very unfavorable price of $41, $4 below the intended $45 Stop. ‘Red’s’ original market value of $4,900 dropped by $800 instead of $400 after the activated Market order filled at the next available price of $41.

–Lesson: Limit orders protect a preferred range of transaction prices. Market and Stop orders don’t protect the transaction price.

Do ‘Circuit Breakers’ Calm Markets or Panic Them?: QuickTake. Nick Baker & Sam Mamudi.The Washington Post 3/19/20, WashingtonPost.com

Appendix: Index methodology

The stock Index is a special sum of weighted prices for many stocks, (w * Price) of many, listed in the stock market. The sum is divided by a special divisor, D.

Index = (w * Price) of many ÷ D

The stocks, their weighting factor (w), and the divisor (D) are proprietary definitions of the Index provider. Repeated calculations of the Index create a string of values that reveal the general volatility and trend of stock prices.

Summary: New investors might find it helpful to understand the basic language of the Stock Market. In this article I discuss the basic vocabulary as it relates to practical ideas for personal investing. Links are provided for further reading about a particular topic.

Investment returns

An investment is the payment of capital to earn a return.The return is a gain (or loss) of value in the investment.Taxes on returns are regulated by the Internal Revenue Service (I.R.S.) and local governments.

Principal: the amount of money invested.

Capital: the cash or goods used to generate income.

Capital gain (or loss): the increase (or decrease) in cash value of an asset.

Dividend: a company’s cash payment to its stockowners.

Interest: the borrower’s cash payment to the lender that is added to the principal of theloan.

Investment portfolio

Financial assets are potential sources of income for investors.Asset classes are groupings of assets that earn income in uniquely different ways.The most popular asset classes are Equities and Fixed Income Securities. Equities earn income by the sale of a security (e.g., shares of a Stock). Fixed Income Securities earn guaranteed interest (e.g., bonds) or guaranteed dividends (e.g., preferred stocks).Securities and investors are regulated by the Securities & Exchange Commission (S.E.C.).

Securities: contracts that require an investment of money to generate profits from the efforts of other people.

Stock: a security that represents part ownership of a company.

Common stock: a security that entitles its owner to vote on important issues, collect dividends, and earn capital gains from the stock market.

Preferred stock: a security that entitles its owner to receive dividends before dividends are paid to owners of the company’s common stock.Preferred stockowners have no voting rights.

Bond: the debt that requires a company to return an investor’s principal, plus interest, by the date of maturity.

A Portfolio is the investor’s collection of financial assets called holdings.By comparison, an Investment Fund is a portfolio of financial securities which are professionally managed on behalf of the fund’s investors.Famous examples are mutual funds and exchange-traded funds (ETFs).An actively managed portfolio generally seeks to earn higher returns than one which is passively managed.The passively managed portfolio seeks to duplicate the returns of a market index.

Market index: a hypothetical portfolio designed to measure the value of a market or market segment.

ETF: an Investment Fund that sells shares of the fund in the stock market.Index ETFs are passively managed.

Stock market

A new stock is issued in its primary market.The primary market is a private assembly of the company’s founders, venture capitalists, and third parties such as banks and advisors.The stock may later be sold by public auction in the secondary market.The secondary market is the familiar stock market where millions of investors, —like us!—,trade cash for stocks and other exchange-traded securities (e.g., ETFs).

Trading orders

The stock market participants includeInvestors who make offers, Brokers who generate orders, and Traders who finalize orders. The broker’s trading platform is a computer program that assists investors with placing trading orders.The platform provides a market “quote” comprised of the current purchasing price (the “bid”), sales price (the “ask”), last-traded price, and latest number of traded shares (the “volume”). On any day there may be millions of orders to buy and sell in the stock market.Orders are filled at the market price determined by an auction of shares conducted by the broker’s trader.Brokers and traders often charge a fee for their services.Custodians are hired by brokers to store traded securities in electronic accounts on behalf of investors.

The simplest trading order, a MARKET ORDER, specifies the number of shares to be traded.Market orders are filled immediately provided the shares are available; otherwise, the order remains open until shares are available.Conditional limit- and stop orders are stored in computers until activated or expired at the end of a period called the time-in-force.The LIMIT ORDER requires an investor to specify a preferred price for the trade.Limit orders are activated when the market price reaches the preferred price and then filled at the preferred price or a better price. Please be aware that a sudden market event could displace the market price outside the limit range of an activated order, in which case the limit order is cancelled unfilled. The STOP ORDER is activated at a specified price after which it is converted to a market order to be filled immediately regardless of the next available price.

Stock market index

Analysts like to follow the price trend of stocks by graphing a representative number called the stock market index.The index rises and falls at any moment according to fluctuations in share prices during stock market transactions.An influential sales surge moves prices downward and a buying surge generally sends prices upward.

Daily index values are strung together to form an observable trend called the market cycle.The long market cycle is comprised of a “bull” market followed by a “bear” market.The short market cycle is either a rally or a correction. Spikes and crashes are brief events caused by a sudden, large change of the index (chart 1).

Bull market: a 20% rise of the market index over 2 months or more.

Bear market: a 20% fall of the market index over 2 months or more.

Rally: a rise of the market index due to a burst of buying that subsides after the money is spent.

Correction: a 10% decline of the market index over 2-10 days.

Spike: a sudden large upward or downward price movement.

Crash: a sudden correction that lasts 1-2 days.

Circuit breakers: programmed halts of trading designed to offset a downward plunge of stock prices.

Chart 1. Long and short cycles of the Dow Jones Industrial Average (“DOW”).

In chart 1, the vertical scale shows values of the DOW Index during a 20 year time period shown by the horizontal scale. The jagged line represents daily fluctuations of market prices. Green, red, and black symbols illustrate the timing of various market cycles and events. The horizontal line of green and red segments portrays 4 long cycles of the DOW Index. After the partial 1st cycle (Jan 2000-Jul. 2001), the complete 2nd (Oct. 2001-Aug. 2002) and 3rd cycles (Sep. 2002-Mar. 2009) show orderly sequences of bull and bear markets. The nearly complete 4th cycle began with a very long bull market of eleven years (Mar. 2009- Jan. 2020) that recently reverted to a bear market at the time of this writing. Chart 1 also shows short cycles of rallies (green triangles) and corrections (red triangles). A few market crashes (black triangles) in Nov. 2008 and Mar. 2020 represent 1-2 day periods of a 10% drop in the Index. Rapid declines of the Index by 7% in one day triggered temporary halts of trading (black circles) known as “circuit breakers”.

Diversification

Stocks are high risk investments with respect to potential capital gains (upside risk) and losses (downside risk). Capital loss occurs when the company declares bankruptcy or its share prices decline. Stock diversification, dollar cost averaging, and dividend reinvestment plans (DRIPs) are effective strategies for managing the common risks of stocks. Monthly purchases of a Stock-index Fund accomplish these strategies. Chart 2 illustrates the potential capital gains from investing in a Stock-index Fund that duplicates a broad market index such as the S&P 500.

Chart 2. Historical prices of the S&P 500 Index.

Assuming that the Fund matches the performance of the S&P 500 Index, the difference between holding the original investment in the Fund without further action (red graph) and augmenting the holding with reinvested shares (blue graph) illustrates the potential benefit of a dividend reinvestment plan.In this example, the benefit became ‘significant’ after 6 years.

Postscript

Stock investing is a time-consuming process that might not interest many people who wish to put their money in the market. They can save time (and money) by investing in a Stock-index Fund that provides an instant portfolio of diversified stocks for long term investment.

The SmallTrades Portfolio holds cash plus an exchange-traded fund (ETF) and a folder of stocks (figure 1).

Figure 1 displays 2019’s year-end composition of the SmallTrades Portfolio. COLUMN HEADINGS: “Ticker” is the trading symbol of the “Security” as listed in the U.S stock exchange.“Mkt Cap” stands for ‘market capitalization’, which is the total market value for all tradable shares of a given security. “Allocation” is the percentage market value of each holding relative to the market value of all holdings in the Portfolio.“Strategy” is the investment strategy.STRATEGY: “Passive” strategy relies on the ETF’s computers to track the value of a selected market index. “Drip” signifies the automatic reinvestment of dividends earned from long term investments in ETFs and stocks.“Growth” stocks are expected to earn long term capital gains.“Swing” stocks are expected to earn short- or long term capital gains based on a pre-defined range of price growth.

Strategy

The investment goal of the Portfolio is to earn an annual rate-of-return that surpasses the performance of the benchmark Standard & Poors 500 Stock Index.One index-ETF dominates the Portfolio’s return with an expectation of matching the benchmark’s rate of return. A subordinate folder of selected stocks is expected to outperform the benchmark’s annual rate-of-return.

Performance

The Portfolio earned a 29.7% total rate-of-return during calendar year 2019.Although the Standard & Poors 500 Index earned a higher rate of 31.5% in 2019, I’m pleased with the Portfolio’s performance for these reasons:

2019 was the first year that the Portfolio’s market value surpassed the initial market value at year-end 2007 (figure 2).As reported in an earlier post, the market value declined in 2008 due to mismanagement, then took 12 years to recover by the process of employing trial-and-error strategies of management. The strategies gradually improved to the current idea of using an index-ETF to earn the benchmark return and supplementing that return with a subfolder of growth stocks.

Converting 2018’s diversified ETF folder to 2019’s single ETF successfully raised the ETF folder’s market value by 33.9% in a single year (figure 3).

Revising both the investment strategy and the composition of 2018’s stock folder raised its market value by 54.9% (figure 3).

Posted by active senior investor

Posted by active senior investor